Federal Reserve Quietly Eliminates Reserve Requirements

Federal Reserve Quietly Eliminates Reserve Requirements

While this happened over two years ago, this underreported Federal Reserve press release had some light shined upon it recently.

Our financial system entered into a new era on March 15, 2020. In a short press release titled “Federal Reserve Actions to Support the Flow of Credit to Households and Businesses”, the Federal Reserve announced multiple actions that they had implemented. While the first three actions undoubtedly had severe ramifications on the American people, it was the fourth action which ushered in a new banking system hitherto undreamt of.

On Friday, June 10, during episode #549 of the popular live, nightly news and politics podcast TimcastIRL, Tim Pool read a comment from an audience member regarding an important but remarkably underreported move that the Federal Reserve made over two years ago back in March 2020. This occurred right around the time our elected officials were claiming “2 weeks to slow the spread” and subsequently attempted to lock us in our homes. After Tim Pool read the comment and appeared shocked, co-host Ian Crossland found the receipts. He pulled up the press release from the Federal Reserve and proceeded to read it aloud for the audience.

Here is a screenshot of the exact words from the Federal Reserve press release.

The Fed decided to issue this press release on a Sunday at 5 PM, a down time for most people. This was clearly a strategic move designed to fly under the radar at a time when regular people were not so worried about a Federal Reserve press release when the media was scaring people so much about a novel Coronavirus that supermarkets had to implement limits on the amount of toilet paper that people were allowed to purchase. Yes, that actually happened.

Before I continue, I would ask you to please take a pause for a minute and think about what zero reserve requirements mean.

We now live in a financial system with a central bank that has no obligation to have any reserves. Actually, we have lived in that system for two years already, but most people aren’t aware of that. I wasn’t even aware of this until recently myself. Theoretically, no bank in the United States has to have a single penny in their vaults because the Fed dropped all reserve requirements to 0% for every tier of banking institution. They can loan out money that does not even exist except as numbers on a screen. The “unlimited money printing” people were complaining about two years ago just became a hell of a lot bigger problem.

It’s no secret that over the last two years that the Federal Reserve has pursued an expansionary monetary policy. They have announced it numerous times, taken every action possible to “expand” the economy, and also claimed that last year’s inflation was transitory on countless occasions.

For anyone not well-versed in central banks and banking issues, here is the situation in a way that is hopefully easier to understand:

Let’s say I start a bank called Brandon Capital. Brandon Capital has $2,000,000 in deposits. Formerly, I would be required to hold 10% of those deposits as reserves, or $200,000. I am able to lend out $1.8 million as loans, which significantly increases Brandon Capital’s bank credit. This is known as a fractional reserve banking system, in which a banking institution is able to lend out most of their deposits as loans, but must keep a ‘fraction’ of deposits as reserves. The fractional reserve banking reserve requirements were designed to act as a buffer against bank runs and is a tool used by the federal reserve when they deem that our economy needs expansion or contraction.

Today, Brandon Capital still has $2,000,000 in deposits. Under the new zero reserve requirement effective March 26, 2020, Brandon Capital may lend out all $2,000,000 of that money and even further increase the bank credit. Here, Brandon Capital has $0 in reserves. This effectively transforms our banking system into an infinite reserve lending system. If there was to be a run on the banks, Brandon Capital would not be able to give a cent to any of their depositors.

(FYI, I will commonly use example scenarios using fictional entities such as “Brandon Capital” when I am discussing complex issues in which an example will make it easier to understand.)

I understand that I may be grossly oversimplifying the fractional reserve lending system versus the infinite reserve lending system, but as I always stress, research these banking practices on your own for a deeper understanding.

We used to have currency based on the gold standard. You can thank Richard Nixon for taking us off the gold standard. We are now so far away from any standard that the majority of our currency does not even physically exist. Any lender can simply add any amount of money to our economy by typing a series of numbers and commas into their computer. This is not a financial model which can be sustained for long, and we are seeing the cracks begin to form in our system. Inflation hit 8.6% recently, the highest level in over 41 years. For many common products, the price hikes have been even worse, especially for meat, gasoline, diesel, fertilizer, and more.

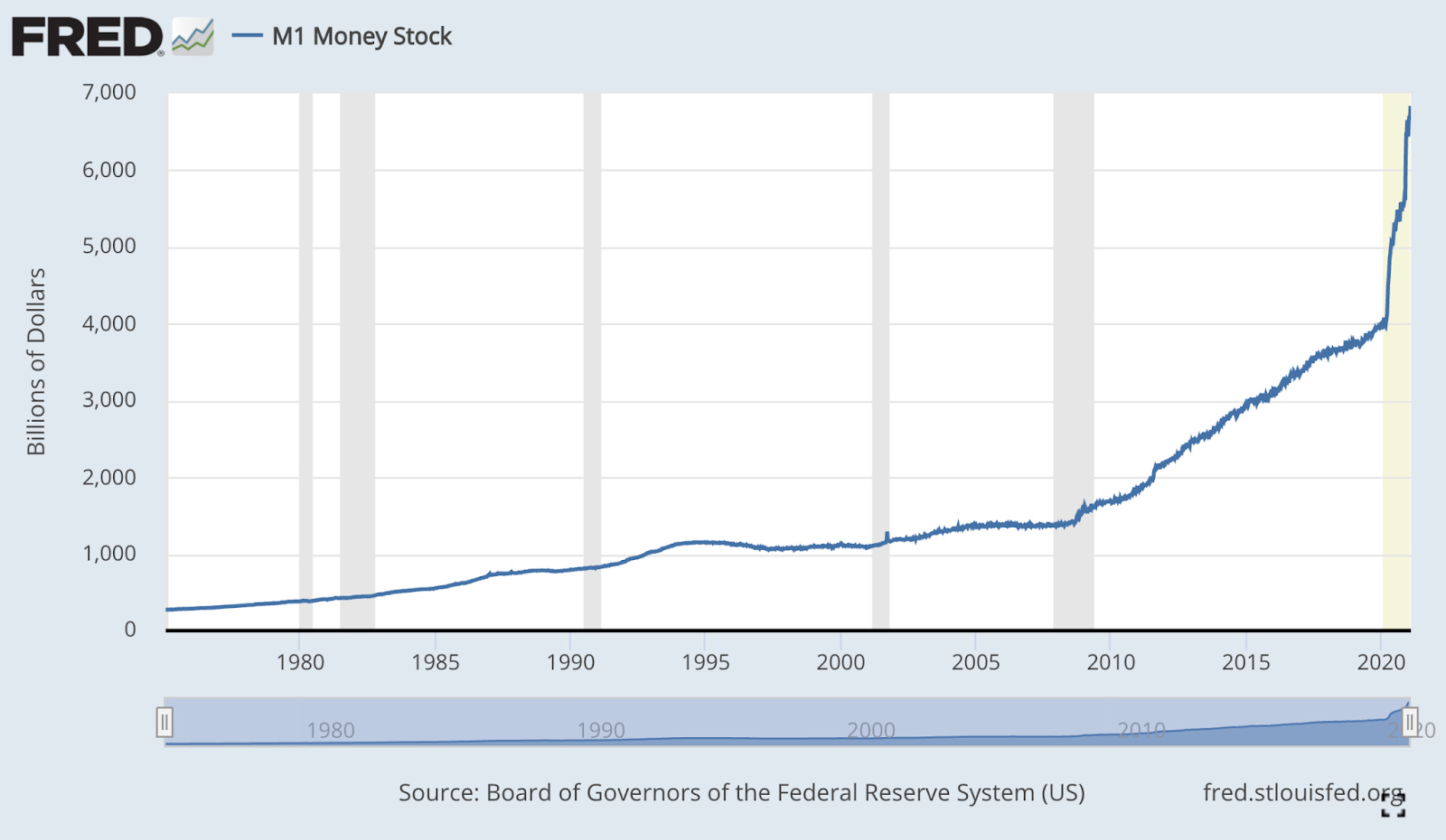

If you take a look at the graph above, you will see that while the monetary supply steadily rose from the 1970s to around 2010, it still remained fairly steady. Beginning in 2010, the money supply began to drastically increase. From around $1.5 trillion in 2010, it rose to just under $4 trillion in early 2020 prior to the lockdowns and removal of the reserve requirement. Following the announcement of the zero reserve requirement, the money supply rose from $4 trillion to nearly $7 trillion in just over one year. More than 40% of all of our USD that has ever existed has been printed since 2020.

I don’t want to be preaching gloom and doom from high upon a soapbox, but it doesn’t take an expert to read between the lines.

As I come to a close, I can just imagine Ron Paul sitting in his house, seeing the tyrannical and senseless policies being passed by unelected officials which are hurting the lower and middle classes, and shaking his head and muttering “I told you so” under his breath. The voters really dropped the ball in 1988, 2008, and 2012.

References:

https://www.federalreserve.gov/newsevents/pressreleases/monetary20200315b.htm

https://www.federalreserve.gov/monetarypolicy/reservereq.htm

https://www.investopedia.com/ask/answers/040115/what-are-some-examples-expansionary-monetary-policy.asp